The host's guide to

Cost Seg + Asset Depreciation

A practical framework and simple overview.

Bola A.

👋✨

👋✨

Agenda

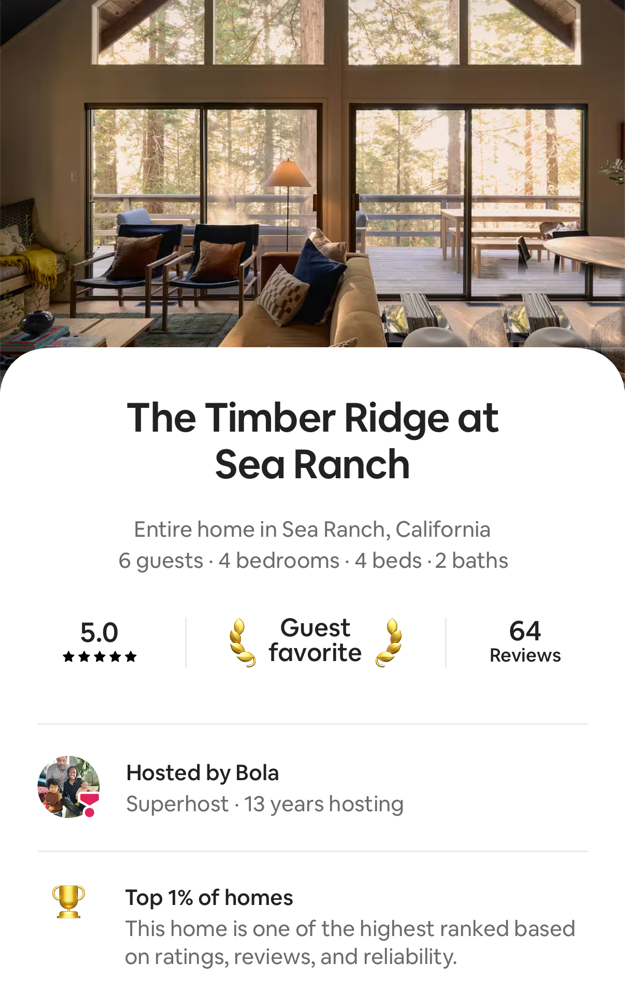

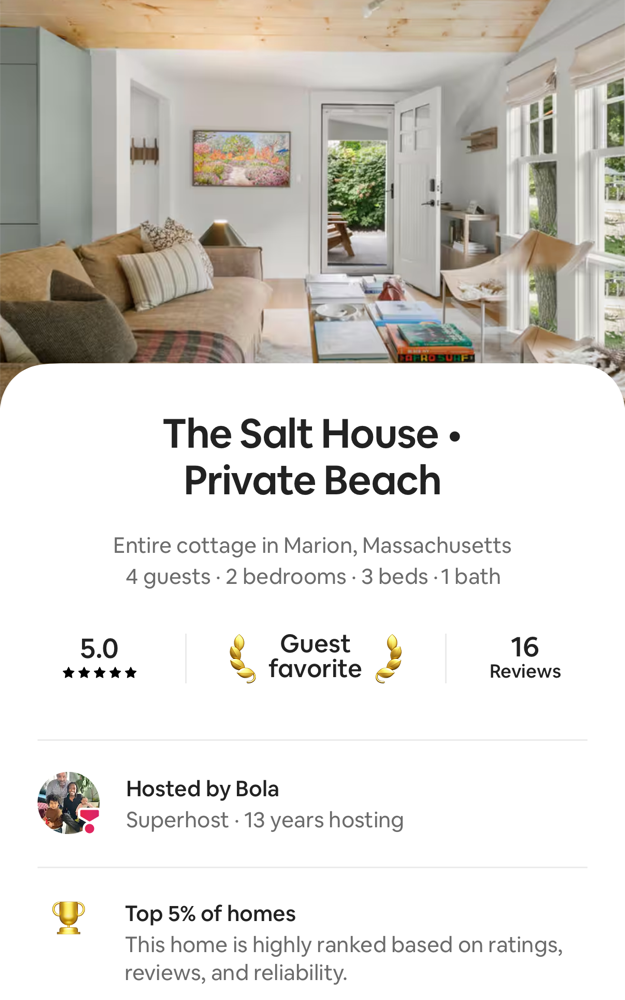

Guess the Y1 deduction

I'll show a property and a few facts. You guess the year-one deduction — then reveal it.

{{ sc.name }}

{{ sc.note }}

Guess the category

For each component, call it: 5-year, 15-year, or 27+. Drop your guess in the chat, then tap to reveal.

Where each one lands

Orange is its class. 5- and 15-year property takes 100% bonus in year one — the structure does not.

Cost segregation = asset depreciation

Depreciation, simply: the loss of a vehicle's value over time — aging, mileage, wear and tear, and market demand.

Different components have different useful life

The things that break down faster than your foundation? You can expense them right away — so you can keep reinvesting and improving the property.

One building becomes multiple asset classes

To use the deduction, you have to qualify

The deduction only helps if your tax situation lets you use it against income. Generally, one of two paths.

Meet Alex

High-tax year.

Planning a remodel.

Alex wants to buy a property and remodel it — but he wants the remodel budget to work harder in year one.

~90% of the budget goes into 5- and 15-year assets

Appliances, lighting, cabinetry, landscaping, outdoor living — the pieces that depreciate fast. Alex spends the remodel budget on the things that write off now, and ends up with the nicest house on the block.

Meet Nancy

Owned for years.

Never ran the study.

Nancy wants to upgrade her rental. She is facing competition and wants a facelift — timed properly, because she cannot float.

Owned it for years? You can still catch up.

Using Form 3115 and a §481(a) adjustment, a look-back study lets you claim the accelerated depreciation you could have taken since the property was placed in service — all in the current year, without amending prior returns.

This is not for everyone

Every smart move here assumes a real tax bill and a scenario where the math actually works.

Your questions

Happy to walk through your scenario, live.

Educational illustration — not tax advice. Figures assume a cost seg study with 100% bonus depreciation and depend on your facts, qualification (STR material participation or REPS), and state conformity. Confirm with your CPA before acting.